General

What is the BAV?

The German pension system is generally based on three pillars:

- state pension

- company pension scheme

- private pension schemes

In recent years, there have been extensive reforms to alleviate the funding problems of the statutory pension insurance scheme and, at the same time, to make occupational pension schemes (also known as company pension schemes) more attractive as supplementary insurance for employers and employees.

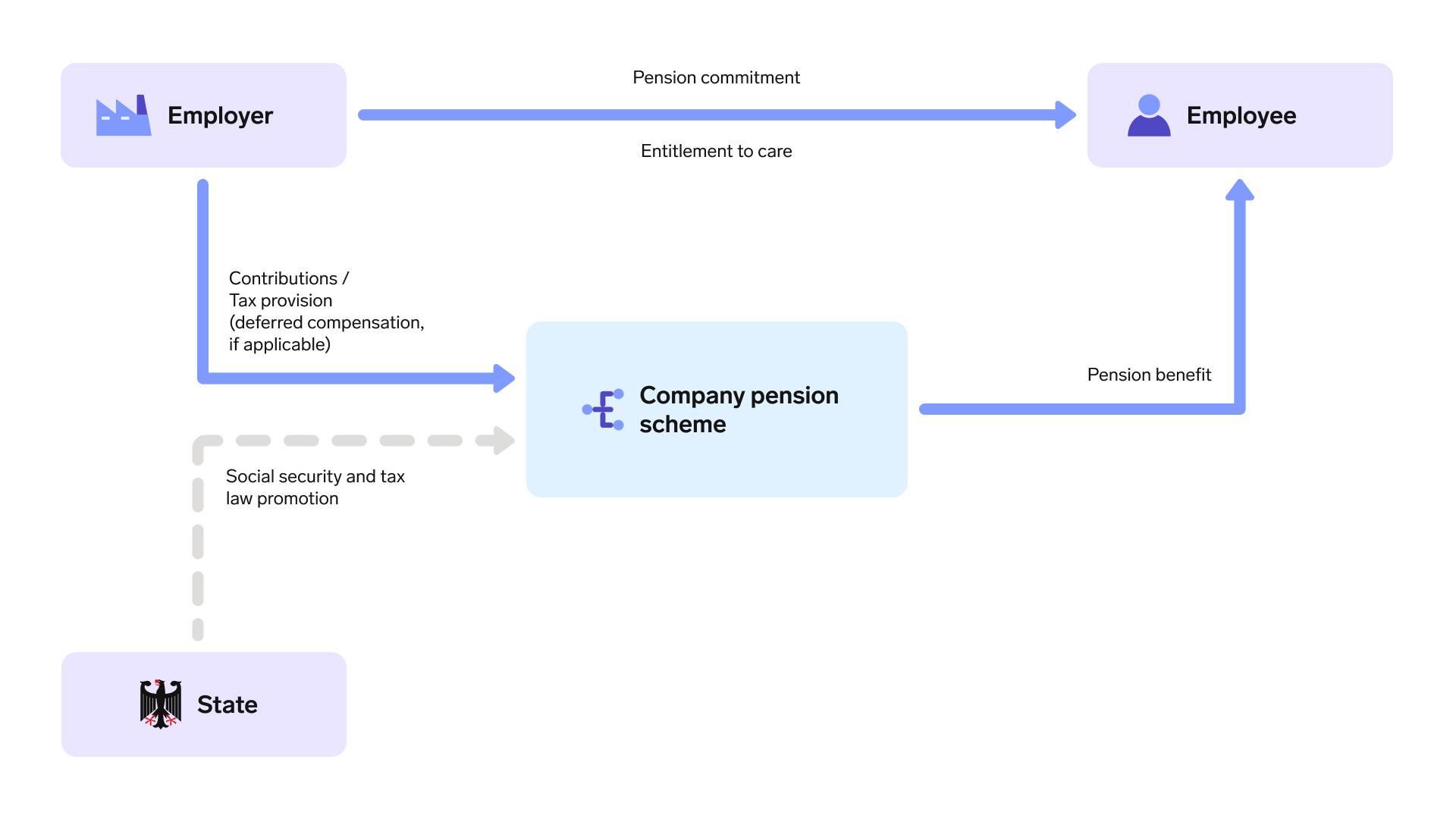

The company pension scheme comprises the financial benefits that employers grant their employees in the event of a claim event. This includes, for example:

- reaching the retirement age

- Disability due to incapacity to work or occupational disability

- in the event of death, provision for surviving dependents

The associated company pensions are a good way for many employees to compensate for losses in statutory benefits and can be financed by employers, employees or by both in a mixed model.

Legal basis

Basis for the regulations

The basis for the regulation of the company pension scheme is the German Company Pension Scheme Act (BetrAVG) of 1974. This Act regulates, among other things, the conditions for a company pension scheme (BAV) to exist; when company pension benefits are retained in the event of a job change or job loss; and how company pensions and entitlements are protected in the case of an insolvency. The Company Pension Strengthening Act came into effect on 1 January 2018.

In addition, the following wage tax regulations must be observed when using the company pension scheme:

- Tax exemption of the company pension scheme is regulated in § 3 No. 56, 63 and 63a .

- The flat-rate taxation of old contracts assigned to direct insurance companies and pension funds is based on § 40b EStG.

- The state subsidy for employers for low-income earners (BAV subsidy amount) is regulated in § 100 of the Income Tax Act .

Legal entitlement to a company pension scheme

Since 1 January 2002, § 1a (1) Clause 1 BetrAVG, employees have a legal right to have their existing salary components converted (deferred compensation) in favor of a company pension scheme. This requires employers to introduce an employee-financed pension scheme as soon as an employee requests this to be done.

With deferred compensation, part of the gross salary is used for pension provision. This is usually cost-neutral for the employer and can lead to savings in social security contributions.

The employee can convert up to 4% of the contribution assessment limit for the statutory pension insurance (West) per year without social insurance contributions:

2024: €90,600.00 * 4% = €3,624.00

The employee must pay at least 1/160 of the pension insurance reference amount into the company pension scheme every year:

2024: €42,420.00 / 160 = €265.13

The employee may voluntarily pay a higher contribution.

Once an employee asserts their right to deferred compensation, the employer must contribute to the deferred compensation by entering into a deferred compensation agreement. The employer has the right to limit implementation to a pension fund society or pension fund. In other cases, the Employee has the right to request to take out direct insurance. However, the employee is not free to choose the insurance company, as an employer cannot be expected to enter into a business relationship with several institutions.

According to § 1a (1a) BetrAVG , employers have to pay 15% of the converted salary as a subsidy if the deferred compensation allows them to save in social security contributions. This rule has applied to all pension commitments since January 1, 2022.

This legal entitlement only applies to employees who are compulsorily insured in the statutory pension insurance.

Note:

Based on the mandatory pension insurance contribution that has applied since 01.01.2013, employees in marginal employment are insured in a statutory pension insurance and are therefore also entitled to deferred compensation. However, if the employee chooses to be exempt from the employer's liability insurance, this legal entitlement expires.

According to § 20 (3) BetrAVG, the employer can introduce an automatic salary conversion for all or certain groups of employees, the so-called options system. This must be regulated in a collective agreement or a works agreement. The employee will be informed at least three months in advance and has the right to object.

Types of company pension commitments

Deferred compensation results in the employee's future salary entitlement being converted into a pension entitlement. This means that the employer has made a pension commitment; the prerequisites for receipt of the pension benefit (for example, the retirement age) from this commitment have not yet been met. The commitment type defines how the benefits that the employer has confirmed for the employee are defined and secured. The employer decides on the type of benefit and thus the content and structure of the company pension scheme.

There are two different types of commitments for company pension schemes:

- Benefit pension scheme: With a defined benefit plan, the employer promises the employee a specific benefit when the insured event occurs. This can be a fixed monthly pension amount or a percentage of a last salary. The employer bears the risks of investing the pension contributions and must provide the promised benefits regardless of the development of the capital markets.

- Defined contribution commitment with minimum benefit: This type of commitment only exists for pension funds, direct insurance, and pension funds. This means that in the event of a benefit event, the employee will receive a minimum benefit equal to the contributions paid, minus certain costs such as risk insurance.

- Defined contribution plan: Here the employer is only obliged to promise a fixed contribution, but no benefit. The subsequent benefit depends on how the saved capital develops.

- Defined contribution commitment (from 01.01.2018): The Company Pension Support Act made it possible to introduce a defined contribution commitment, under which the employer is only obliged to pay contributions to a pension fund, pension fund or direct insurance, but is not liable for a certain pension amount. To this end, the parties to the collective agreement must sign a collective agreement regarding a company pension scheme in the form of a defined contribution commitment. The amount of the company pension depends solely on the success of the capital investment. For coverage, a security contribution should be agreed in the collective agreement according to § 23 (1) BetrAVG . In the case of deferred compensation, the employer must pass on 15 percent of the converted salary as a subsidy if this results in savings in social security contributions.

Mandatory employer contribution to the company pension scheme

General Information

Since 01.01.2018, § 23 (2) BetrAVG has a legal requirement for employers with a defined contribution commitment to pay an additional 15% of the converted salary to the pension fund if they can save social security contributions.

Note:

Defined contribution commitments can only be found in collective agreements.

Since 01.01.2019, employers have also been required to make a subsidy contribution for all newly entered deferred compensation agreements in favor of a pension fund, pension fund or direct insurance, provided that they save social security contributions. Since 01.01.2022, this also applies to existing contracts.

Note:

This is a collective bargaining right, which means that collective bargaining regulations remain in force even if they are less favorable. Newer collective agreements may also deviate from this to the detriment of the employee.

The amount of the mandatory subsidy for the employer depends on the amount of savings in social security contributions. This can vary depending on the employee’s salary and the level of the contribution assessment ceiling (BBG).

There are three possible options for calculating the subsidy from 2022:

- The employer's mandatory subsidy is paid into a newly agreed contract.

- The total amount increases by the employer's compulsory subsidy in an existing contract with the exclusive method.

- In the inclusive method or self-calculation, the previous salary conversion amount is reduced by the statutory subsidy.

Mandatory subsidy of 15%

The salary is:

- within the contribution assessment ceiling for health and long-term care insurance

- within the contribution assessment ceiling for pension and unemployment insurance

This means that the employer saves on social security contributions in all areas of SV and thus has to pay a mandatory subsidy of 15% based on the amount converted.

Example

An employee is paid a salary of €3,500.00. From January 2017, a deferred compensation of €250.00 in direct insurance was agreed.

The direct insurance contributions are tax-free up to 8% of the contribution assessment ceiling in the RV (West) and up to 4% of the contribution assessment ceiling RV West (social security contributions). This leaves 2024:

- €7,248.00 per year and €604.00 per month tax-free

- €3,624.00 per year and €302.00 per month free of social security contributions

| Without deferred compensation | In the case of deferred compensation | |

| €3,500.00 | €3,250.00 | |

| Health insurance (7.3% + 0.8%) | €271.25 | €251.88 |

| Pension insurance (9.30%) | €325.50 | €302.25 |

| Unemployment insurance (1.3%) | €45.50 | €45.25 |

| Long-term care insurance (1.7%) | €59.50 | €55.25 |

| Total contributions | €701.75 | €651.63 |

This would result in an employer saving of €50.12 on SI contributions .

The employer must agree with the employee and the insurance company on the form in which the subsidy should be paid.

Option 1

The direct insurance contribution is increased by the employer's subsidy. The employer's mandatory subsidy is €37.50 (€250.00 * 15% = €37.50). The total contribution is now €287.50 (€250.00 + €37.50).

Option 2

The calculation is the same as for Option 1, except that the mandatory employer contribution is paid into a newly concluded contract.

Option 3

The total contribution paid to the direct insurance remains the same. The deferred compensation is reduced only by the amount of the compulsory employer's subsidy. There are two possible ways of calculating this.

- In hundreds: €250.00 / 115% * 15% = €32.61 AG subsidy; €250.00 - €32.61 = €217.39 deferred compensation

- Per hundred: €250.00 * 15% = €37.50 employer contribution; €250.00 - €37.50 = €212.50

Since the SI savings are higher in all three options than the subsidy of 15%, the employer must pay this in full.

Reimbursement with 10.6%

The salary is:

- only within the contribution assessment ceiling for health and long-term care insurance

- outside the contribution assessment ceiling for pension and unemployment insurance

This means that the employer only saves on social security contributions for pension and unemployment insurance. They only have to pay a mandatory contribution of 10.6 % (9.3 % pension insurance and 1.3 % unemployment insurance) based on the converted amount.

Example

An employee is paid a salary of €5,600.00. From January 2024, a deferred compensation with the highest possible tax- and social insurance-free contribution of €302.00 in direct insurance was agreed. The employer uses the internal calculation (in hundreds) for the subsidy payment.

The direct insurance contributions are tax-free up to 8% of the contribution assessment ceiling in the RV (West) and up to 4% of the contribution assessment ceiling RV West (social security contributions). This leaves 2024:

- €7,248.00 per year and €604.00 per month tax-free

- €3,624.00 per year and €302.00 per month free of social security contributions

| Without deferred compensation | In the case of deferred compensation | |

| €5,600.00 | €5,298.00 | |

| Health insurance (7.3% + 0.8%) | €416.59 | €416.59 |

| Pension insurance (9.30%) | €520.80 | €495.41 |

| Unemployment insurance (1.3%) | €72.80 | €69.25 |

| Long-term care insurance (1.7%) | €87.98 | €87.98 |

| Total contributions | €1,098.17 | €1,069.23 |

This would result in an employer saving of €28.94 on SI contributions . The Insich calculation results in the following employer contribution: €302.00 / 110.6% = €28.94 employer contribution; €302.00 - €28.94 = €273.06 conversion amount.

Note:

The employer has the option of paying a higher subsidy on a voluntary basis.

No mandatory employer contribution

The salary is:

- outside of the contribution assessment ceiling for health and long-term care insurance

- outside the contribution assessment ceiling for pension and unemployment insurance

This means that the employer does not save any social security contributions and is therefore not obliged to pay an allowance. However, it is possible to do so voluntarily.

Note:

The same tax and contribution regulations apply to the employer contribution as to the deferred compensation.

Subsidy for low-income earners according to § 100 EStG

What is the subsidy amount?

With the Company Pension Support Act, the support amount for low-income earners pursuant to § 100 EStG also came into effect on 1 January, 2018. This is a state subsidy for an employer's contribution to a company pension scheme, in addition to the salary that is already owed for employees on a low income. This does not include the employer's contribution of 15% that is already mandatory and paid by employers for saved social security contributions.

In this case, employers receive a direct tax subsidy of 30% if they offer employees a company pension scheme up to a certain income limit. The employer must pay at least a calendar-year contribution of €240.00 to a pension fund, pension fund or direct insurance. Contributions for direct commitments Provident funds are not eligible.

Note:

Employers are not obliged to apply for this support amount.

Income limit amounts

The aim of the occupational pension subsidy is to expand the company pension scheme for low-income employees. With this in mind, the state subsidy is only granted to the employer for employees whose taxable salary does not exceed €2,575.00 per month .

The minimum contribution of €240.00 per year is only taken into account if the income limit is not exceeded at the time the contributions are paid. The following salary components are not taken into account when calculating the income limit:

- Tax-free salary components such as Surcharges for Sundays, public holidays and night work

- Other payments, for example, vacation or Christmas bonuses

- Non-cash benefits that fall within the €50 tax-free limit

- components of flat-rate taxed salaries according to §§ 37a, 37b, 40 EStG and § 40b EStG

According to the BMF letter of 12 August 2021 , the subsidy can only be applied for employees who are in their first employment period. This also includes employment without an entitlement to a salary (For example, during parental leave, care leave or if you receive sickness or short-time work benefits). If an employee changes jobs in the course of a year, the company pension scheme can be used again up to the maximum amount, regardless of whether it was already used in the old employment. However, this does not apply to a business takeover.

Note:

Part-time employees, those in marginal employment and trainees can also benefit from this company pension scheme.

Amount of funding

The company pension scheme is granted. Employers pay at least €240.00 into a company pension scheme during a calendar year. The upper limit for annual contributions is €960.00. The state subsidies 30% of this amount, resulting in a minimum of € 72.00 and a maximum of €288.00 per year for company pension schemes.

Example of how the company pension scheme is calculated

In July 2024, the employer takes out direct insurance for a part-time employee. The employee's monthly gross salary is €1,800.00, which is below the monthly low-income limit of €2,575.00. The employer results in annual contributions being paid for the first time in July 2024 in the amount of:

- Case 1: €200.00

- Case 2: €400.00

- Case 3: €1,000.00

paid to the insurance company. The employer applies for the company pension scheme support amount.

| Case 1: The employer is not granted the subsidy amount because the annual minimum contribution of €240.00 was not paid. | Case 2: The funding amount is €120.00 (30% of €400.00). | Case 3: The employer is granted the maximum subsidy amount of €288.00 (30% of €960.00). |

Implementation methods of the company pension scheme

Overview of implementation methods

When it comes to implementing the company pension scheme, the employer can generally choose between five different investment forms, which can be categorized into internal and external implementation methods. These differ in terms of tax and social security law.

| Internal implementation methods | External implementation methods |

|

|

Internal implementation methods

With the internal implementation methods, the employer them self takes care of the implementation of a company pension scheme. The options are:

Direct commitment

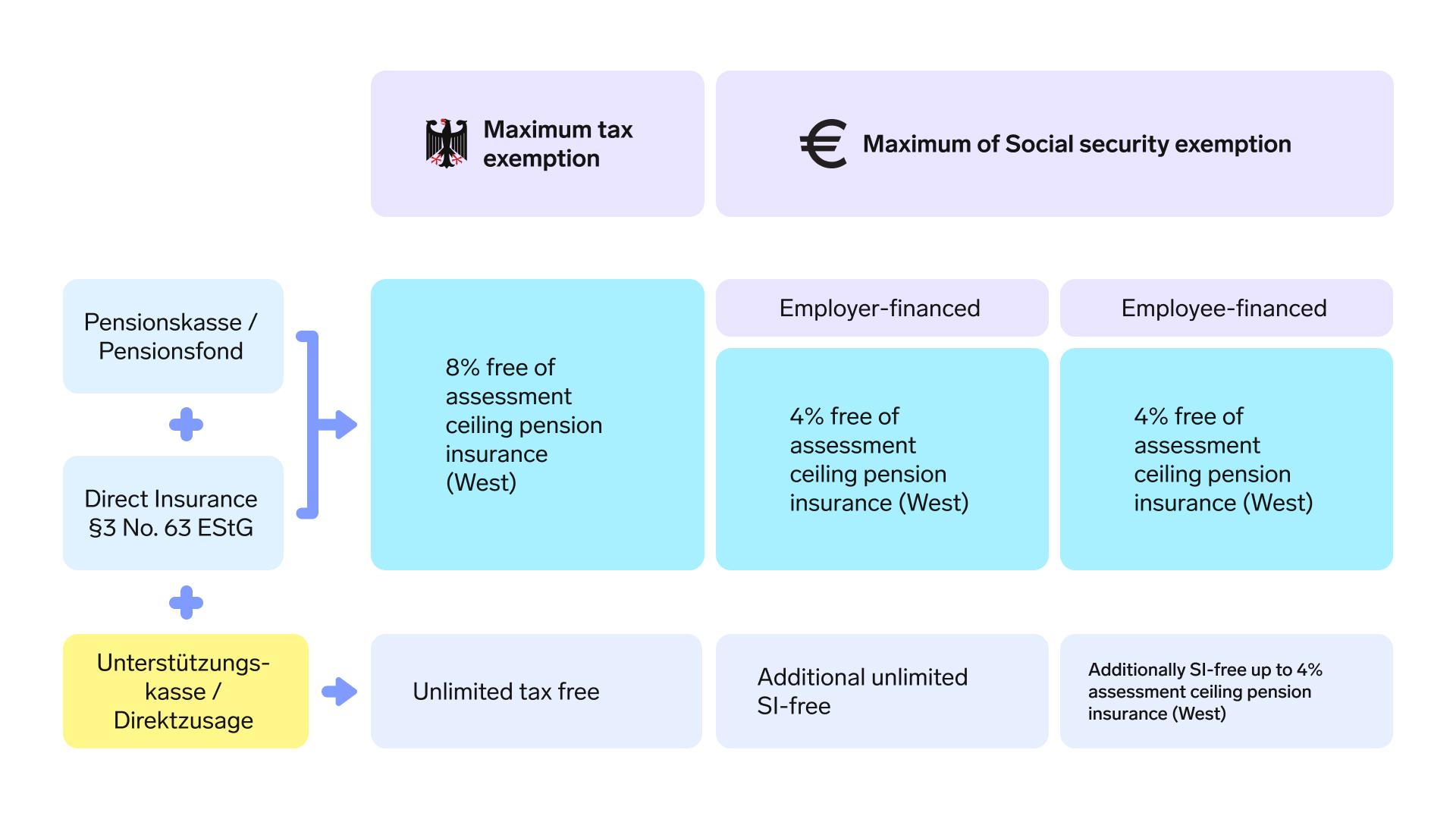

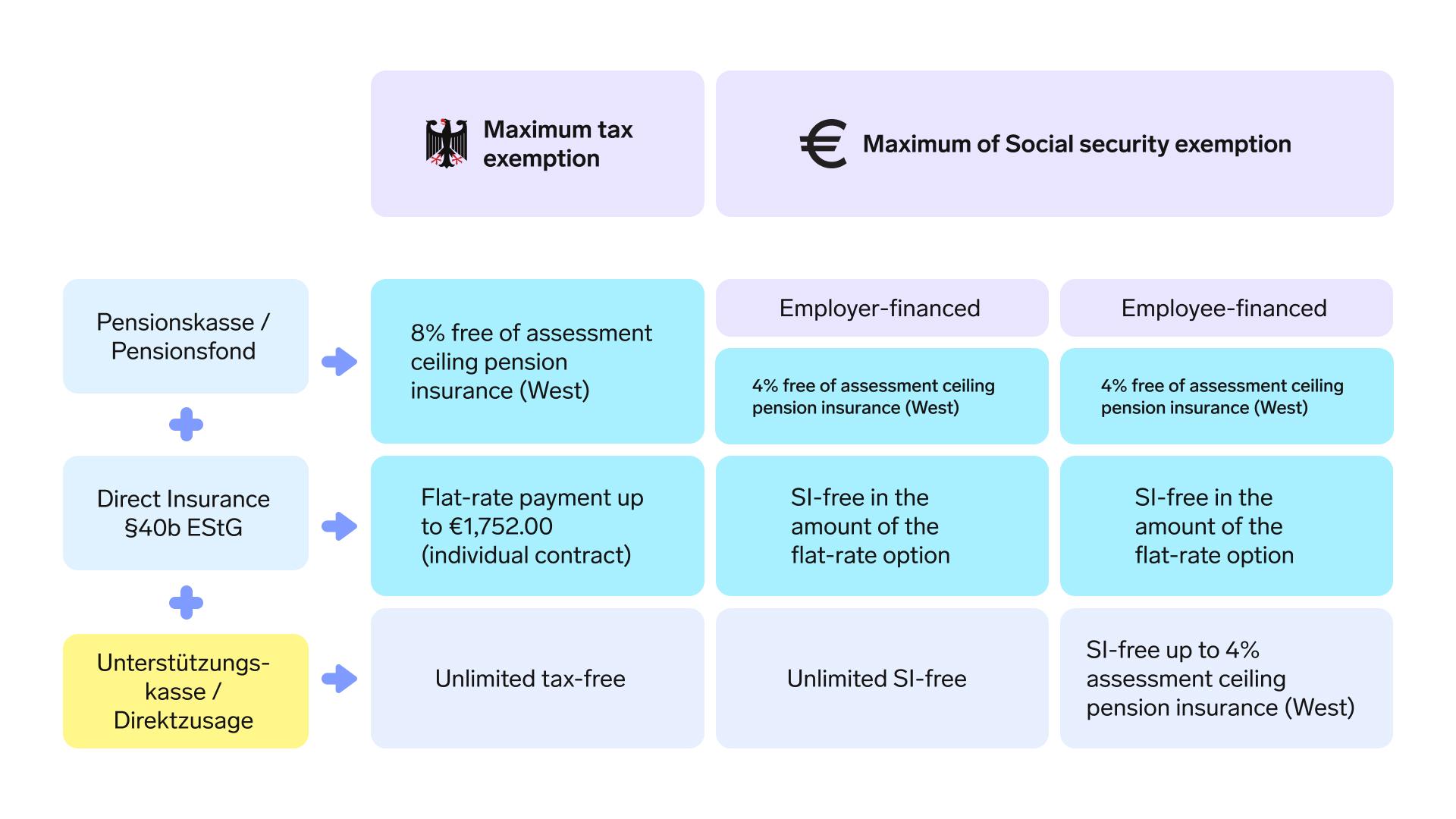

Direct commitments (internal pension commitments) are a direct commitment from the employer for provision of a benefit; this is granted without an external partner. With a direct commitment, the employer undertakes paying the employee certain benefits when an insured event occurs.

The employer ensures that pension entitlements are protected by setting up pension accruals in the tax balance and by taking out corresponding pension insurance . In the case of insolvency, the employees' entitlements from a direct commitment by the Pensions-Versicherungs-Versicherungskassen VVaG (PSVaG) are covered.

Unterstützungskasse (Provident fund)

Provident funds are the first form of company pension scheme and have their origins in the 19th century. They are considered to be legally independent pension schemes that are independent of employers and take over the implementation of company pension schemes for them. However, they do not grant the employee a legal entitlement to future benefits.

If the provident fund is not able to provide the agreed benefits, the employer is responsible according to§ 1 (1) 3 BetrAVG . This means that the employee is not directly entitled to benefits from the provident fund. In the event of an employer's insolvency, the Pensions-Versicherungs-Versicherungssocial insurance (VVaG (PSVaG)) secures the employees' entitlements.

Income tax treatment

When contributions are paid to a direct commitment or provident fund, employers do not initially grant the employee any financial benefits in the event of a claim. There is therefore no taxable income during the savings phase . As a result, the contributions to the internal implementation methods are fully tax-free.

A salary is only generated later, in the payment phase of the pension benefits. These are fully subject to wage taxation.

Social insurance-related treatment

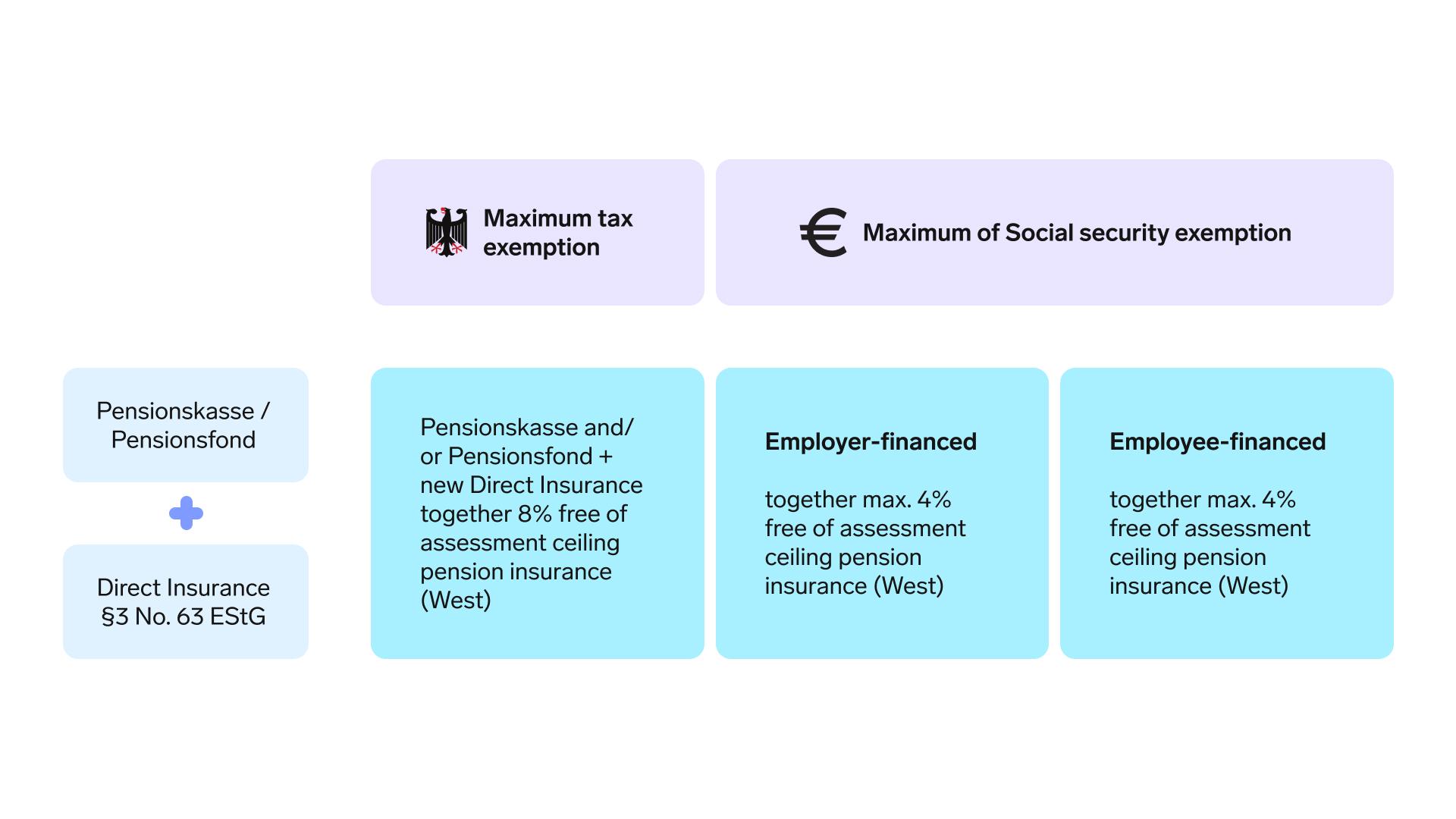

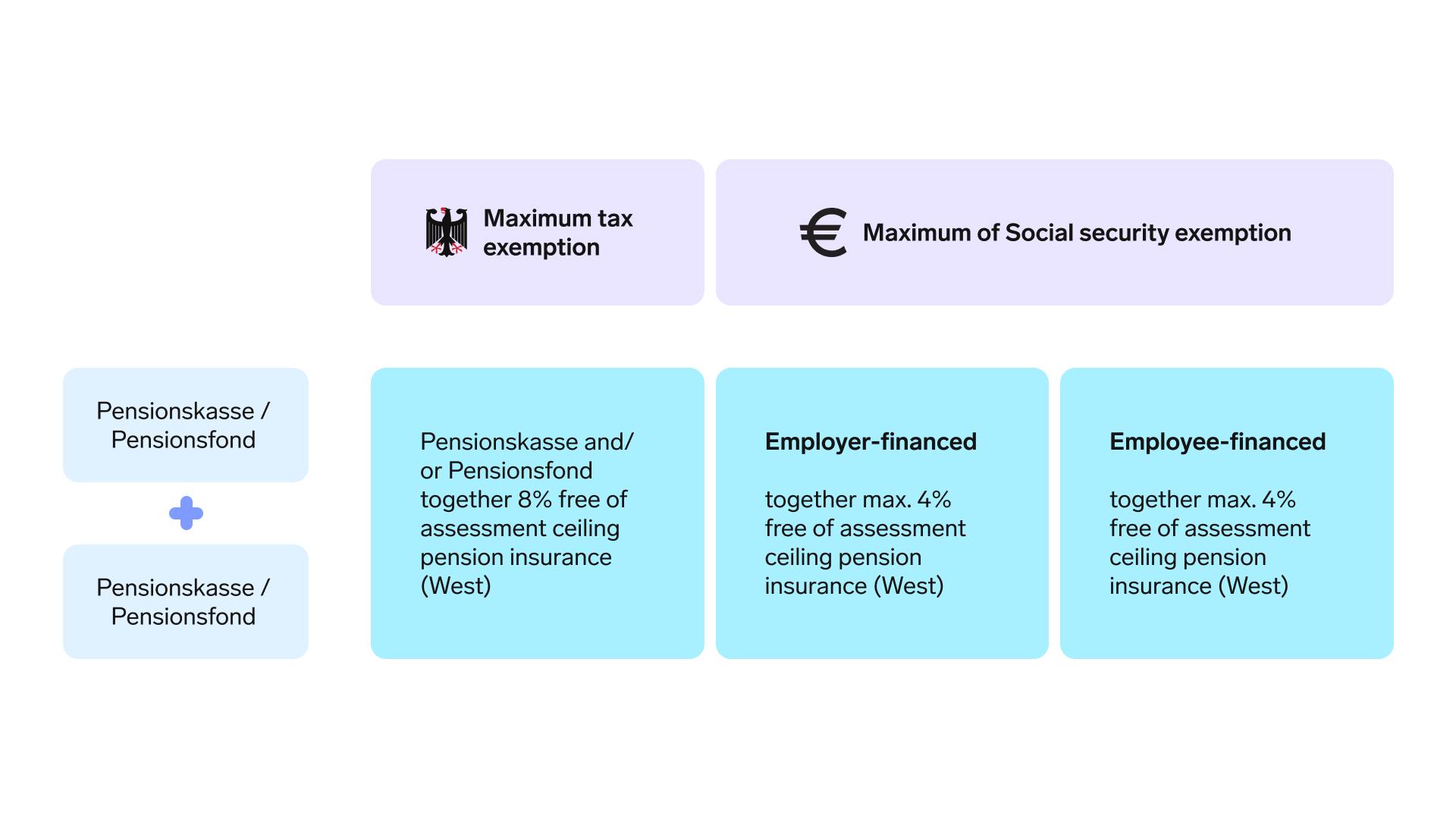

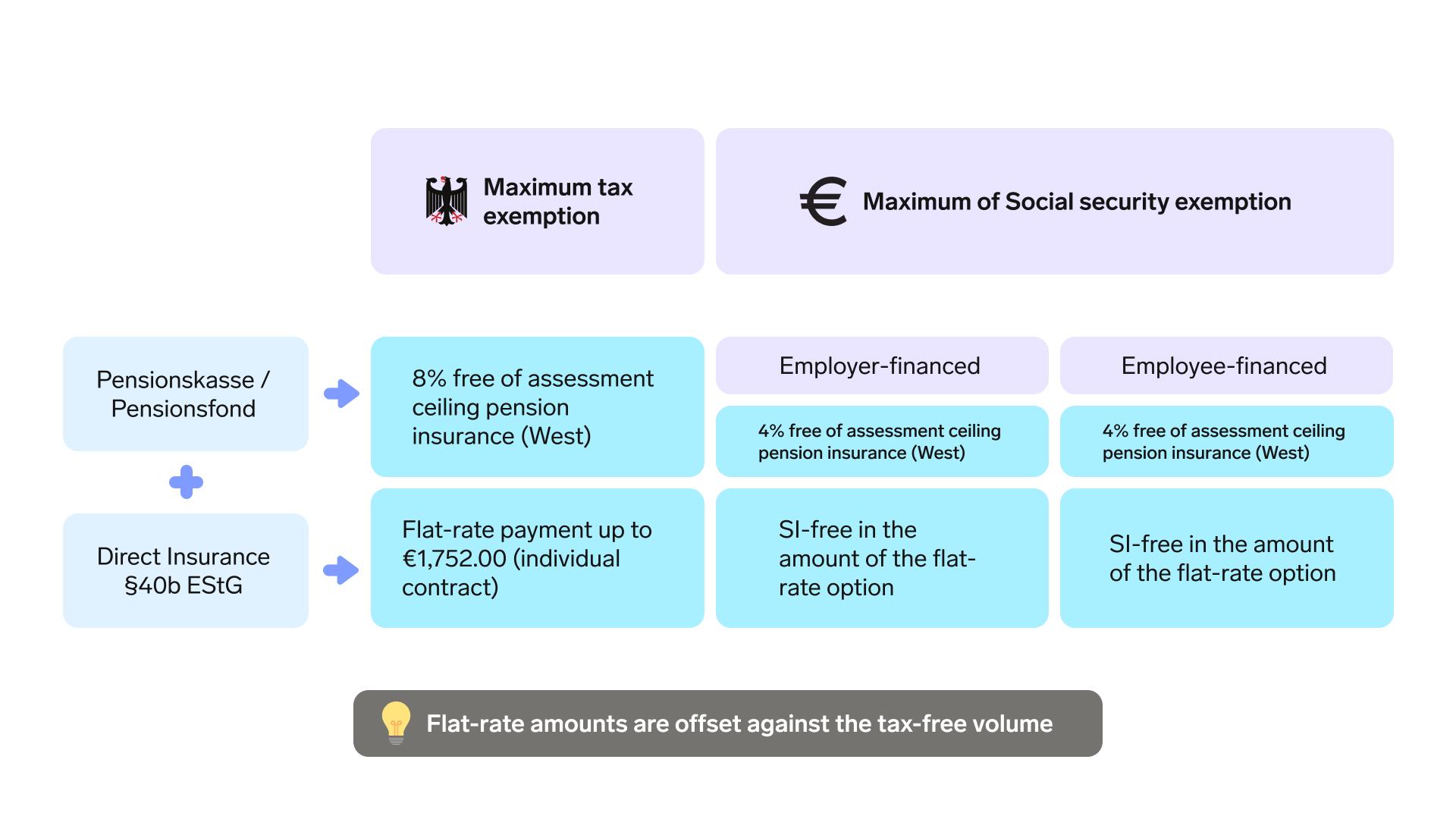

In accordance with § 14 (1) Sentence 2 SGB IV , parts of the salary that are converted for a direct commitment or provident fund provision do not count in the calculation of the employee's remuneration for social insurance. As long as this converted amount does not exceed 4% of the annual contribution assessment limit for general pension insurance (West) (2024: €3,624.00 per year), it remains exempt from social security contributions.

However, any amount that exceeds this 4% must be considered as remuneration and is subject to mandatory social security contributions. If the contributions to social security system are purely employer-financed, there is no social security obligation

Contributions to health and long-term care insurance are accrued during the payment phase, and these are only paid by the employee.

External implementation methods

With external implementation methods, employers hand over the implementation of the company pension plan to an external insurance company or pension provider which grants the employee a legal right to a pension benefit in the case of a claim event. Here, the contributions and gratuities that the employer makes for setting up a company pension scheme are considered employee wages. Additionally, the state supports these contributions to securing the employees' future with several tax benefits. Here, the options are:

Direct insurance

Direct insurance is considered to be the simplest and most popular type of company pension scheme. It works in a similar way to private life insurance, which the employer takes out for their employee. The legal basis for this is § 1b (2) BetrAVG.

The most important features of direct insurance are:

- The employer as the policyholder takes out an individual or group life insurance contract in favor of the employee (insured person).

- The employee or their eligible surviving dependents are the beneficiaries.

- The employee has unrestricted and irrevocable subscription rights.

Pensionskasse (Pension fund)

According to §1b (3) Clause 1 BetrAVG , a pension fund is a legally recognized pension institution that grants the employee or their surviving dependents a legal right to benefits in the event of a claim. They may be operated in the legal form of a public (insurance) company or a mutual insurance association (VVaG). In contrast to direct insurance, the employee who is a member of the pension fund is the policyholder.

Pensionsfonds (Pension fund society)

The pension fund, which came into effect on 1 January 2002, is the most recent of the five implementation methods for company pension schemes. Pursuant to § 1b (3) BetrAVG , a pension fund is a legally independent institution that grants employees or their surviving dependents a legal entitlement to their benefits.

The legal definition is the same as that of a pension fund. In contrast to a pension fund, a pension fund is not an insurance company, but is organized in the form of a stock corporation or a pension fund association and has relatively more freedom with the investment of their assets. The aim here is to achieve a higher return.

Income tax treatment

Tax exemption for funded company pension schemes

Based on § 3 (63) EStG , employer contributions to a pension fund, pension fund or direct insurance during the first employment period are tax-free up to a maximum of 8% of the annual contribution assessment limit for the West German pension insurance (for 2024: €7,248.00). . The relevant contribution assessment limit (West) for the calendar year is always relevant.

Contributions exceeding the tax-free maximum are subject to regular income tax.

Note:

The annual allowance applies to the entire calendar year, regardless of the duration of the employment relationship or the payment of contributions that were only made during part of the year. They can use the maximum amount again if they change employers. However, this does not apply to a business takeover.

For old contracts before 1 January, 2005, the tax-free amount is reduced by contributions to funded pension funds and contributions to direct insurance that, according to §40b EStG, F. should be taxed at a flat rate of 20 %.

Flat-rate taxation according to § 40b EStG

For direct insurance and capital-covered pension funds, under certain circumstances, it is possible to charge income tax at a flat rate of 20% up to €1,752.00 in accordance with § 40b EStG old. F.

For a flat rate to be applied, the employee must have taxed at least one contribution to a flat-rate company pension scheme before 01.01.2018 . However, this only applies to company pension scheme agreements that were made before 01.01.2005 . If these conditions are met, the employee can continue to use the flat rate for their entire life. Contract changes, new contracts, changes to the pension commitment or a change of employer are irrelevant. The decision for or against using the flat rate has far-going consequences for the tax assessment of the pension benefit. Contributions that are taxed at a flat rate are not considered to be supported, with the result that the based pension benefits do not have to be taxed in full.

Note:

Contributions to a pension fund cannot be taxed at a flat rate.

Taxation of Pension Benefit

Benefits that become available when the insured event occurs (for example, old-age, death or disability) or in the case of a compensation for pension entitlements must be taxed as other income in the former employee's income tax assessment.

The taxation of these benefits during the payout phase depends on the tax treatment of the contributions during the savings phase:

- Pension benefits that are based on tax-free contributions or are supported by state subsidies such as retirement provision bonuses or additional deductions for special expenses (subsidized contributions), and the benefits are always subject to full tax deductions.

- Pension payments based on contributions that are taxed at a flat rate or individually according to the electronic income tax deduction characteristics (ELStAM) (so-called non-subsidized contributions) are usually only partially taxable. Capital payments also do not fully constitute taxable income.

Social insurance-related treatment

Contributions to an external implementation method are generally exempt from social insurance up to 4% of the annual contribution assessment limit of the pension insurance (West). The important feature is that the payment must be made later as a life-long pension.

Time off of contribution is not relevant here, whether the financing is done by the employer, through deferred compensation by the employee, or through mixed financing. The same applies to whether the deferred compensation takes place from an ongoing salary or a one-time salary payment.

Note:

In the case of mixed financing (combination of employer and employee contributions), the allowance is only available as a total. Privately paid contributions always have precedence.

In addition, flat-rate taxed contributions according to § 40b EStG are also exempt from social security contributions up to an amount of €1,752.00.

Contributions to health and long-term care insurance are due during the payment phase and are borne by the employee only.

Option to combine several company pension schemes

It is possible to combine several implementation methods for the company pension scheme at the same time. The following points must be noted in the process:

- Tax and social security regulations apply uniformly to all new commitments.

- The tax and social security exemption can only be claimed once in all external implementation methods, up to the maximum limit.

- Flat-rate taxation in accordance with § 40b EStG and tax exemption in accordance with § 3 no. 63 EStG can take place at the same time, but contributions taxed at a flat rate must be credited to the tax-free amount.

Recording models for tax and social security allowances

Which models are available?

The tax-free amount of €7,248.00 is an annual allowance that can be used in full, even if the employment is not for the entire calendar year or contributions are only paid for part of the year. Employers have two options to waive tax-free amounts.

-

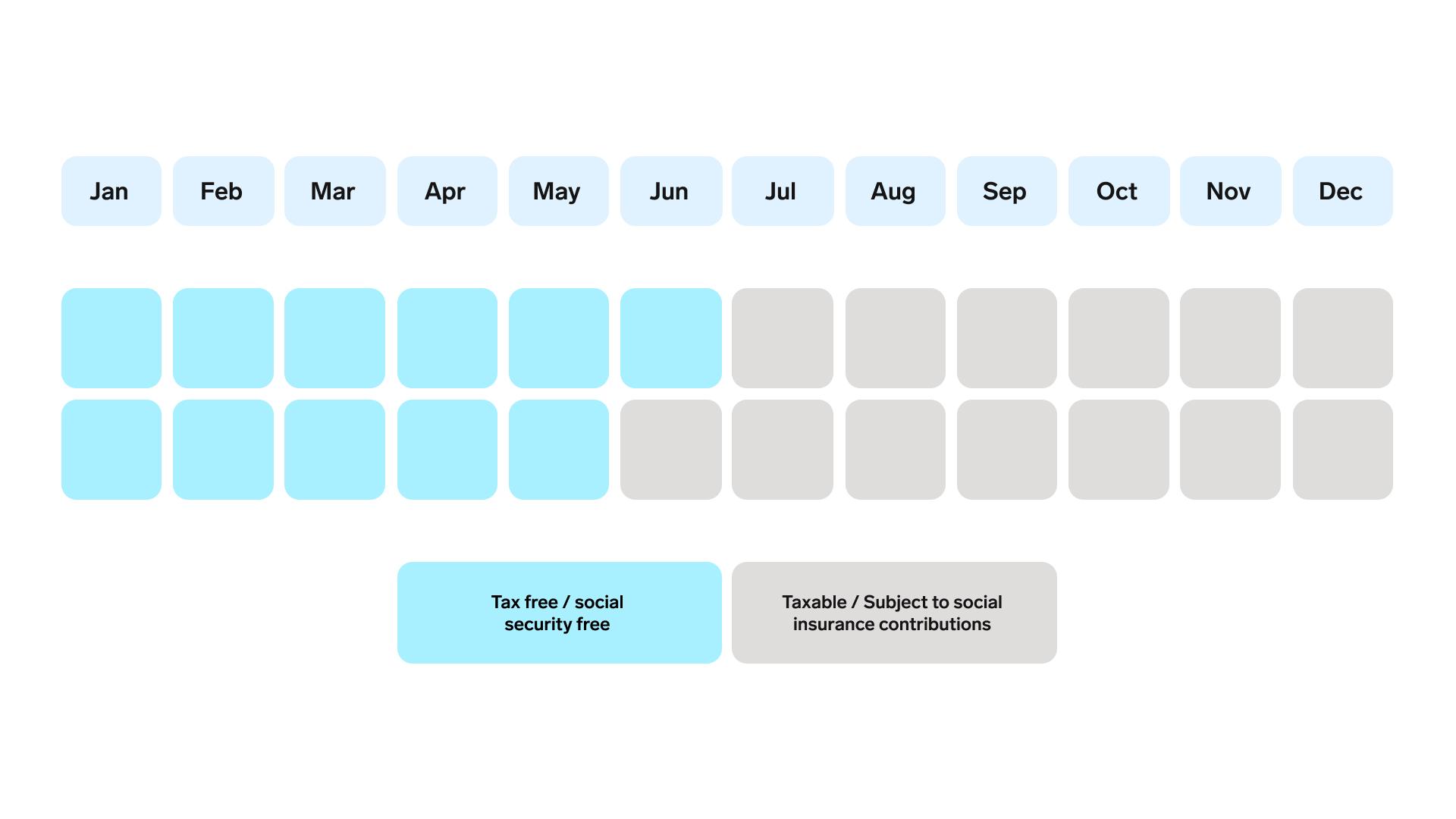

En-bloc (annual use/exhaustion model): With this model, deferred compensation is exempt from tax and social security contributions until the annual allowance has been exhausted. It only becomes subject to tax and/or social security contributions once the employee has exhausted this allowance. This is the most commonly used model in practice.

-

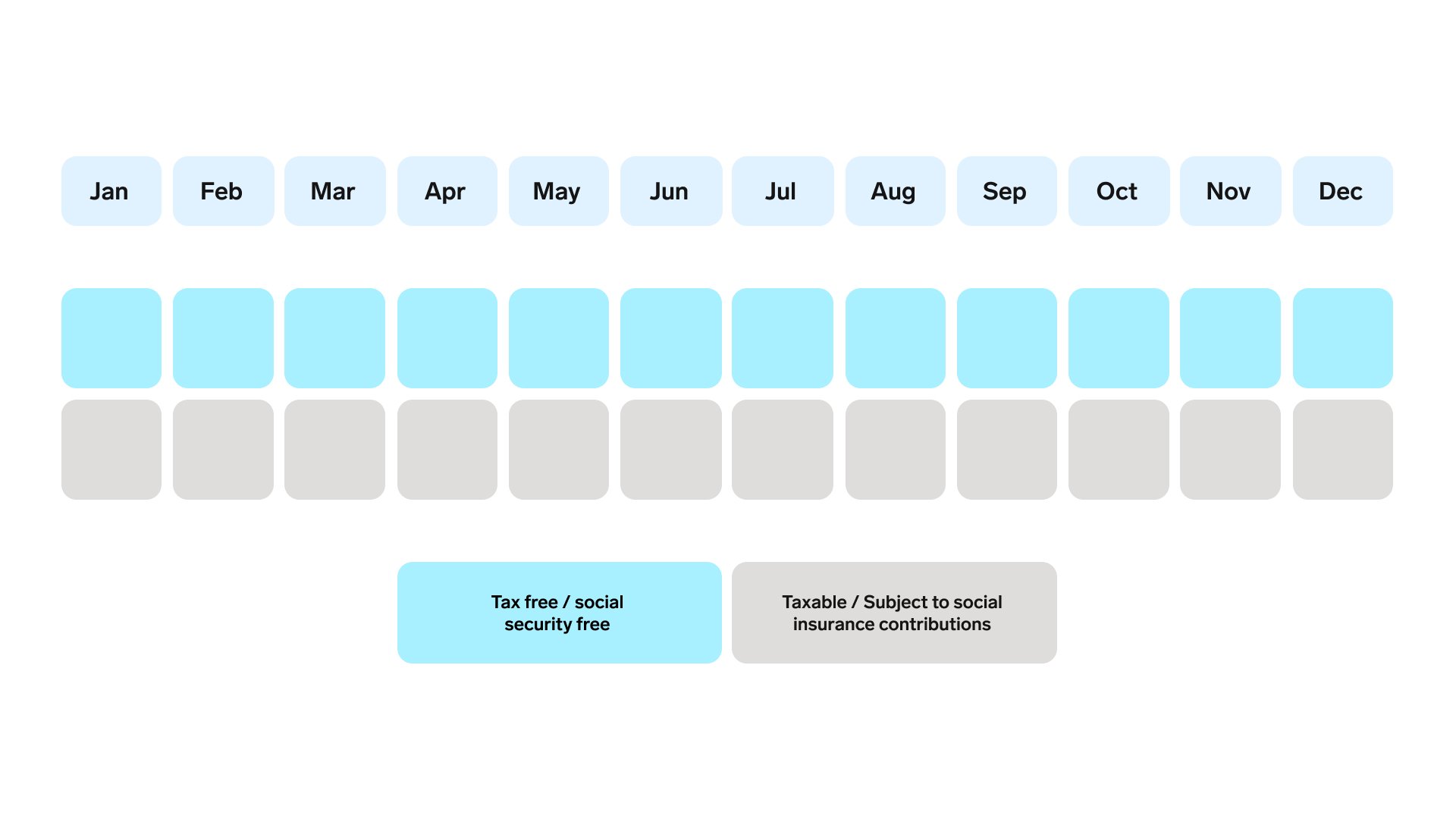

Pro-rata (monthly use/distribution model): With the distribution model, the tax- and social security-exempt allowance is distributed evenly over the individual months. This means that in the case of higher contributions to the BAV, a portion is generally exempt from tax and social security contributions, while the remainder is subject to tax and social security contributions and is either taxed at a flat rate or individually depending on the contract.