What is a contribution statement?

A contribution statement is a documented list of the, usually actual, amount of social insurance contributions for the current payroll month that the employer is required to pay to the relevant collection center by the due date. The collection center is the employees' health insurance, and in the case of marginal employees, the Minijob-Zentrale.

Contribution statements may only be transmitted to the health insurers' data receipt workplaces electronically via data transfer from a system-approved payroll accounting program or using a fill-out help such as the SV-meldeportal.

Legal basis

The structure of the data sets for the submission of contribution statements is based on § 28b (2) SGB IV and § 256 (1) Clause 4 SGB V. The National Association of Statutory Health Insurance Funds provides additional information.

zero contribution report

If there are no contributions in a month, e.g. an employee is on sick pay and as a result does not receive any salary, a so-called zero contribution statement is created. This must also be sent to the collection center responsible.

Statement of continuous contribution

If the employee always receives the same salary, e.g. due to a fixed monthly salary, the employer has the option of submitting a statement of continuous contribution. This only needs to be adjusted if the amount to be paid changes, e.g. if there is a change to the employee's salary, contribution rates or contribution assessment ceilings.

Correction of a contribution statement

Adjustments to contributions from previous months can generally be included in the contribution statement for the current month. In this case, any overpaid contributions are offset against each other. Alternatively, you can cancel the contribution statement that you have already sent and submit a new contribution statement for the same period of time.

Structure of a contribution statement

Header of the contribution statement

The header of the contribution statement contains the following information:

- Employer's address

- the payroll period

- Contribution account number of the employer or the company registration number

- The employer's tax number

- Legal domain (East or West)

Note:

If the employer has to pay contributions for employees in both the old and the new federal states, two separate contribution statement data sets are created for East and West Germany. The separate legal entitlements of East and West Germany remain in place until at least 2025.

Main section of the contribution statement

The actual main part of the contribution statement contains the contribution group keys and the correspondingly assigned amount.

If the employer may reimburse the employer's expenses for continued payment of remuneration in the case of sickness (U1) or for maternity expenses (U2), the amount will be deducted from the subtotal. This results in the total contribution to be paid for social security or the credit.

Note:

Flat-rate contributions and the uniform flat-rate tax for marginal employees are shown to the Minijob-Zentrale in a separate contribution statement.

Contribution rates for 2025

| Contribution rate | Employee share | |

|

Health insurance general contribution rate (with entitlement to sick pay) reduced contribution rate (without entitlement to sick pay) average additional contribution |

14.6% 14.0% 2.5% |

7.3% 7.0%

|

|

Pension insurance general Knappschaft Bahn-See |

18.6% 24.7% |

9.3% 9.3% |

| Unemployment insurance | 2.6% | 1.3% |

|

Long-term care insurance no children no children in Saxony with child 1 with child in Saxony 1 |

4.2%

3.6%

|

2.4% 2.9% 1.8% 2.3% |

1 Since 01.07.2023, a contribution deduction for the 2nd to 5th child has to be taken into account when calculating the long-term care insurance contribution (Pflegeversicherungsbeitrag).

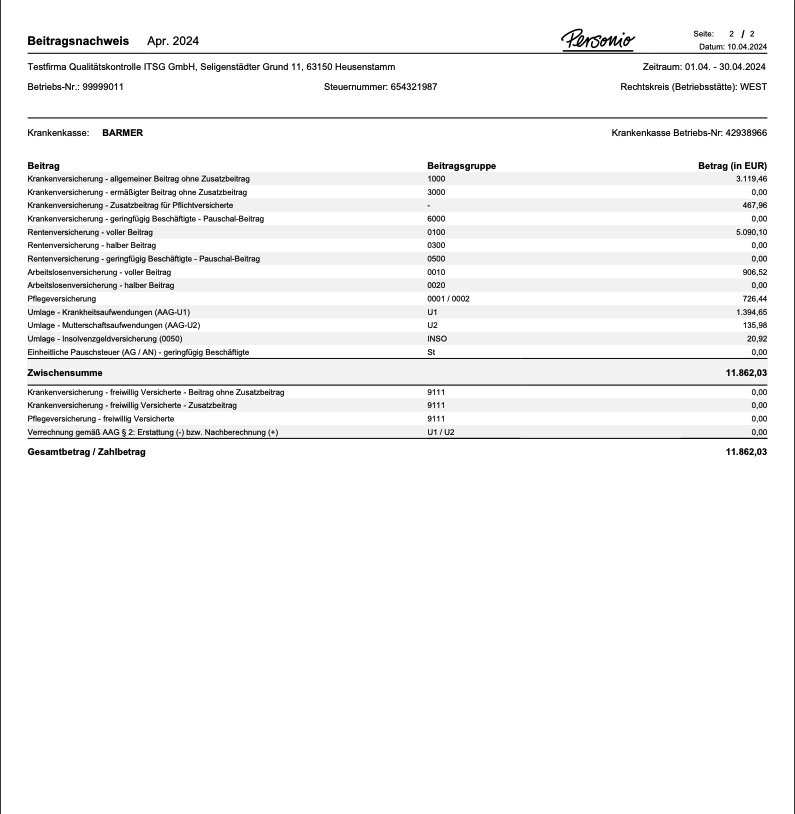

Sample contribution statement

Due dates for the contributions and contribution statement

Overview of contribution due dates and contribution statements

The basis for the due date of the contribution statements is the § 23 (1) SGB IV. There, it is specified that the social insurance contributions (health, long-term care, pension and unemployment insurance) of employees who are subject to mandatory insurance and calculated based on the current month's salary are due no later than the third from the last bank working day.

If the employee's remuneration is due and the payroll has been completed, contributions shall be paid when they become due in the actual amount of the contribution liability.

The national due date for contribution statements for the current month can also be calculated from the contribution due date according to § 28f (3) SGB IV . Employers must send their contribution statements for the current month electronically, at the latest two working days before the contributions are due. The certificate must be received by 12:00am on the fifth-last bank working day. If the employer submits a contribution statement too late, the collection center/health insurer is free to estimate the relevant salary until the certificate has been submitted.

Due dates for 2025

| Contribution Month 2025 |

Contribution statement appointment (2 days before due date) |

When contributions are due (second from last bank working day) |

| January | 27.01.2025 | 29.01.2025 |

| February | 24.02.2025 | 26.02.2025 |

| March | 25.03.2025 | 27.03.2025 |

| April | 24.04.2025 | 28.04.2025 |

| May | 23.05.2025 | 27.05.2027 |

| June | 24.06.2025 | 26.06.2025 |

| July | 25.07.2025 | 29.07.2025 |

| August | 25.08.2025 | 27.08.2025 |

| September | 24.09.2025 | 26.09.2025 |

| October |

24.10.2025 1 27.10.2025 |

28.10.2025 1 29.10.2025 |

| November | 24.11.2025 | 26.11.2025 |

| December | 19.12.2025 | 23.12.2025 |

1 applies to federal states where the Reformation Day is a public holiday

Estimation process for social security contributions

What is the social security contribution assessment process?

In some cases, employers are not able to carry out contribution payroll with the actual contribution amount. These cases occur mainly when the employer, e.g. the employee's monthly salary is calculated based on the hours worked, and the total hours for the current month are not yet known at the time the contributions become due. There are two options:

- According to § 23 (1) Sentence 2 SGB IV, contributions must always be paid in the expected amount.

- According to the so-called simplification rule according to § 23 (1) Sentence 3 SGB IV , contributions are paid in the amount of the previous month.

In both cases, the remaining contribution is due on the third-last bank working day of the following month.

The employer who does not know the actual contribution debt will calculate the social security contribution based on the expected contribution debt or transmit the actual value for the previous month at their own discretion. The employee is not permanently bound by their decision on how the target contributions are determined. You can switch between them after each payroll month. However, the switch must be documented in a verifiable way in accordance with § 9 (1) Sentence 1 No. 10 BVV .

Expected amount of contributions

Calculation and documentation

In the contribution debt to the expected amount procedure, the employer must calculate the amount in such a way that the remaining contribution is as low as possible and the final contribution debt is as similar as possible. No simple discount should be displayed here.

This calculation is based on the contribution target. This is created as a fictitious calculation based on the expected employee's salary. Changes such as new hires, terminations, working days or hours must be taken into account. The expected contribution liability must be noted separately for each employee and each collection center.

The target contributions, which are shown on the contribution statement for the current payroll month, include:

- the expected contribution liability for the month in which the employment that generated the remuneration was performed

- the remaining contribution or, if applicable, the compensation for an over payment from the previous month

The remaining contribution does not lead to a retroactive adjustment of the previous month's target contributions due and thus not the contribution statement. The allocation of the contribution to the salary remains unchanged, and the remaining contribution is therefore assigned to the original month in which the work is performed and its associated contribution factors.

Note:

The criteria and methods used to calculate the expected contribution debt must be documented in accordance with Section 9 (1) Clause 1 No. 10 BVV .

Consideration of variable and one-time salary components

When calculating the expected contribution liability, variable salary components must also be taken into account. If these are regularly paid late and the employer is therefore not able to take them into account in the same payroll period, they can be assigned to the salary for the next month or the one after that. These include, for example, compensation for overtime or bonuses for work on Sundays, public holidays, or at night.

In the case of one-off payments of remuneration, the entitlement to contribution accrues according to Section 22 (1) Sentence 2 SGB IV as soon as these have been paid. However, when determining the expected contribution liability, the employer must always check whether the one-off payment will be made in the current month with sufficient certainty. He knows this id R. at the time it determines the expected contribution liability.

Simplification Rule

In addition to calculating the expected contribution deficit, the employer also has the option, according to § 23 (1) Sentence 3 SGB IV , of paying the total social security contribution in the amount of the previous month's target on the due date. This is referred to as the simplification rule.

Payroll, in contrast, does not depend on regular changes such as onboarded and offboarded employees and variable payments.

The previous month's target and the actual contribution owe are also settled with the payroll of the following month. The remaining contribution is due by the third to last bank working day of the following month at the latest.

Note:

In cases where no target date for the previous month is known (e.g. when setting up a new business, the simplification rule cannot be applied. Here, the expected contribution liability for the current month is to be determined.

If the target contribution is "0" in the previous month, e.g. because the only employee in the company is entitled to sick pay, this value will also be applied for the current month when the simplification rule is applied. If there are no differences to be made up for the previous month, the employer must send a contribution statement with zero amounts to the collection center.

Consider one-time salary components

The simplification rule does not apply to a one-time remuneration (see Draft of a Second Administrative Support Act in Federal Council document 437/16, justification for article 7). Here, the regulation of § 23a (1) SGB IV applies, and one-off payments must be taken into account in the month in which the employee receives them. Contributions that are due in the previous month on a one-off basis for remuneration are deducted from the previous month's contribution debt when calculating the contribution debt for the current month.

If, on the other hand, a one-time payment is to be made in the current accounting month, the expected amount of the one-off payment must be added to the contributions from the current salary based on the previous month.